The AI funding numbers in 2026 are so large they’ve stopped feeling real. Let’s make them real. Here’s where the money is actually going, which categories are winning, which are quietly dying, and what the investment patterns tell us about where AI is headed.

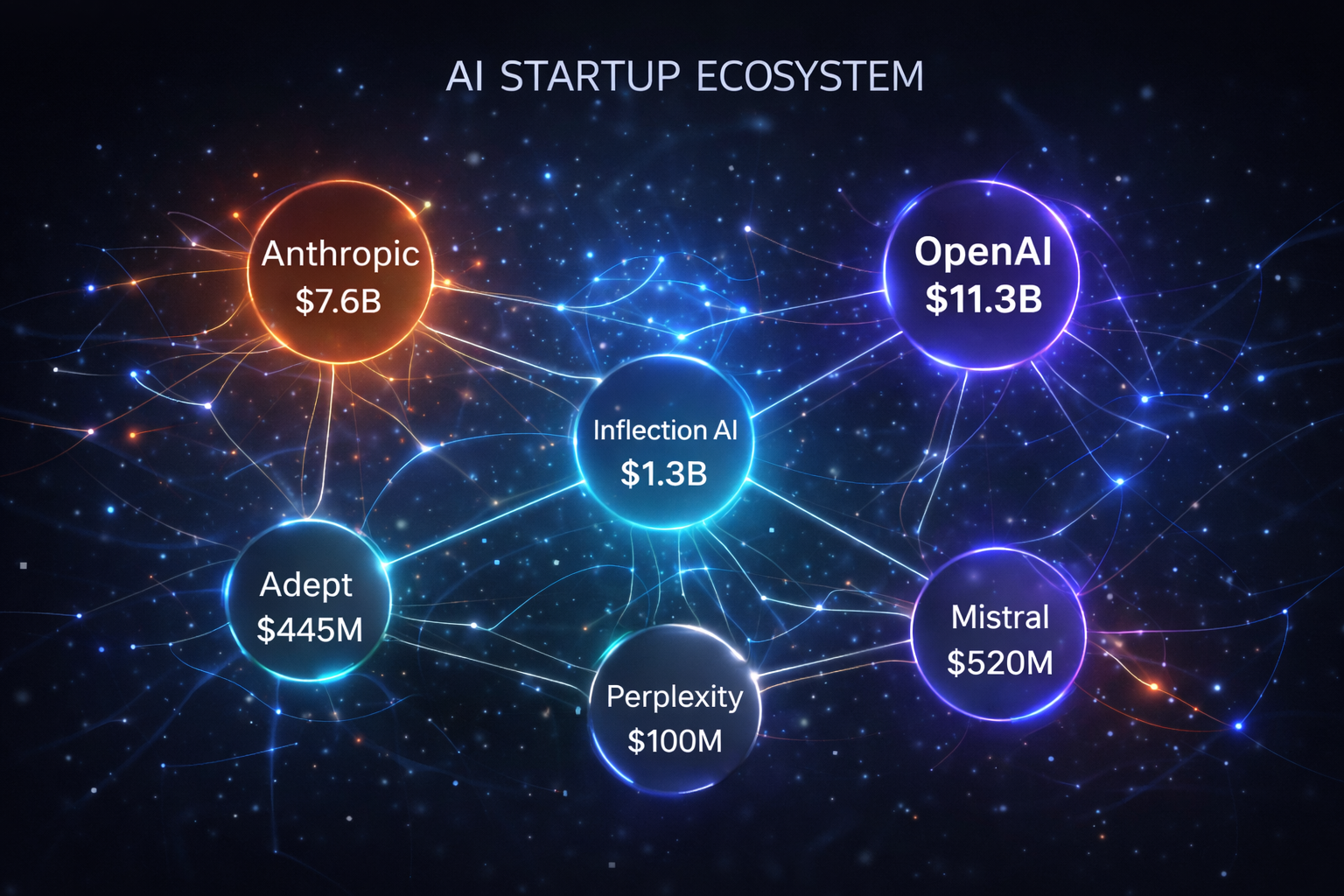

On February 27, 2026, OpenAI closed a $110 billion funding round — the largest private venture capital raise in history. At a $840 billion post-money valuation, OpenAI is now the most valuable private company ever recorded. Amazon committed $50 billion and became OpenAI’s exclusive third-party cloud partner as part of the deal. OpenAI’s annualised revenue has exceeded $20 billion.

These are not normal startup numbers. They’re numbers from a different category of company — something that functions as infrastructure, with geopolitical implications and national security dimensions that go well beyond software.

But OpenAI is just the most visible story. The AI funding landscape in 2026 is extraordinarily active across multiple tiers, from the frontier labs raising in the tens of billions, to the mid-market enterprise AI companies consolidating around specific verticals, to the seed-stage startups trying to find defensible positions in a market dominated by increasingly capable incumbents.

Understanding where the money is going — and why — tells you more about where AI is actually headed than any technology forecast.

The Frontier Labs: Infrastructure, Not Startups

OpenAI, Anthropic, and xAI have crossed a threshold where calling them startups is technically accurate but functionally misleading. They are operating as critical national infrastructure, and their fundraising reflects that.

OpenAI — $840B post-money valuation, $110B raise. 810 million monthly active users. Over 1 million enterprise customers. Revenue exceeding $20 billion annualised. IPO targeting Q4 2026 at a near $1 trillion valuation.

Anthropic — $380B valuation following its $30B Series G. Claude has become the dominant choice for enterprise AI deployment in regulated industries, driven by its constitutional AI approach and strong safety posture. Anthropic economists at Anthropic itself have published some of the most sober research on AI’s labour market effects — a credibility move that differentiates it from competitors in enterprise sales.

xAI — $20 billion Series E at a $100+ billion valuation. The Grok model, running on the Colossus supercomputer (approximately 200,000 GPUs), is expanding into enterprise and developer markets. The merger with SpaceX creates potential for space-based computing infrastructure that no other AI company can match.

The pattern across all three: capital concentration is accelerating. OpenAI and Anthropic alone absorbed $140 billion in Q1 2026 — an amount that reflects institutional treatment of these companies as essential technology infrastructure, not venture bets.

The Breakout Categories of 2026

Beyond the frontier labs, three investment categories are clearly dominant in early 2026.

Humanoid Robotics — The Year’s Biggest Surprise

Figure AI validated humanoid robotics as an investment category in a way nobody had managed before. Its Amazon deployment — 20,000 units initially, with 50,000 units on order from Mercedes — represents the first genuine commercial-scale humanoid robot deployment.

Figure 03 prototypes are demonstrating 50% faster task completion across manipulation and navigation benchmarks. Production is scaling at 1,200 units per month, targeting 5,000 per month by Q4 2026. The combined order pipeline exceeds 70,000 units, representing a $14 billion+ revenue pipeline through 2029.

The investment community has responded accordingly. SkildAI raised $1.4 billion in a Series C — a signal that investors are now betting on the robot foundation model layer as a separate, investable category. The humanoid robotics sector is projected to draw $20 billion+ in funding in 2026 alone.

Voice AI — Quietly Becoming Infrastructure

ElevenLabs reported $330 million ARR with enterprise adoption from Deutsche Telekom, Revolut, Meta, and Salesforce. Following a $130 million raise at a $1.3 billion valuation, the company is being positioned by investors as core enterprise infrastructure — voice AI sitting alongside text LLMs as a foundation layer for human-computer interaction.

Deepgram, a competing voice AI platform, raised at a $1.3B valuation as well. The category is consolidating around a small number of players who are embedding their APIs in enterprise software stacks — a dynamic that favours early movers with distribution.

AI Infrastructure and Compute

Nscale raised $2 billion at a $14.6 billion valuation for European AI data centres — a signal that the geographic distribution of AI compute is becoming a strategic concern alongside the technical distribution. The nuclear power partnerships announced by Microsoft, Google, and Amazon in 2025 are now moving toward execution, as AI data centre energy demands require power solutions at a scale that the grid wasn’t designed to support.

The European Counter-Narrative: Mistral

France’s Mistral AI has become the clearest European alternative to the US AI labs, and its trajectory in 2026 is worth examining in detail.

Mistral raised €1.7 billion at an €11.7 billion post-money valuation — with Dutch semiconductor giant ASML joining as a lead investor, a notable signal about European industrial interest in maintaining AI infrastructure sovereignty.

The Le Chat business platform, Mistral’s enterprise product, offers advanced memory capabilities and extensive third-party integrations at no cost — a direct competitive challenge to OpenAI’s enterprise tier. The company is explicitly positioning itself as “Europe’s answer to OpenAI,” with the regulatory and data sovereignty advantages that come with European jurisdiction at a time when the EU AI Act is establishing tiered compliance requirements.

Mistral’s open-weight model strategy has earned it significant developer goodwill globally — including quiet adoption in US products where companies prefer not to be named. The gap between frontier Chinese and Western open-source models is narrowing to weeks rather than months, and Mistral is benefiting from the same dynamics that make open-source AI increasingly attractive.

What’s Quietly Dying: The Middle-Market Squeeze

The AI investment landscape in 2026 has a structural problem that isn’t getting enough coverage: the middle market is being squeezed.

The frontier labs are building capabilities so broad and so fast that the “generic AI wrapper” category — products built on top of GPT or Claude with minimal differentiation — is becoming genuinely difficult to defend. When ChatGPT adds native coding capabilities, Codex-integrated tools lose their moat. When Claude adds document analysis, document-analysis startups face pressure. When Gemini integrates with Google Workspace, productivity AI startups built for Google users have a harder story to tell.

VCs are explicitly predicting that enterprises will concentrate AI spend on fewer vendors in 2026. Companies without moats — proprietary data, vertical depth, or meaningful switching costs — are facing funding headwinds regardless of how good their product is.

The clear winners in the middle market are vertical AI companies — startups with deep domain expertise in a specific industry, training on domain-specific data, building for compliance environments that generic models can’t navigate. Healthcare coding AI, legal document AI, manufacturing quality control AI, financial compliance AI — these categories are raising well because they offer something the frontier labs can’t easily replicate: domain-specific accuracy in regulated contexts.

Vertical AI models reduce error rates by 20-40% compared to generic models across many sectors, according to Industry Research data. Over 70% of enterprises require AI outputs to comply with domain-specific rules and regulations — a requirement that increasingly favours specialised vertical players over general-purpose incumbents.

The IPO Queue and What Comes Next

The public market pathway for AI companies is opening in 2026, with several major events on the calendar.

OpenAI is targeting a Q4 2026 IPO at a near $1 trillion valuation. Databricks is targeting Q2. CoreWeave — the GPU cloud provider — filed for an IPO in Q2. xAI (merged with SpaceX) is targeting June for a public offering.

These IPOs matter beyond the companies themselves. They will establish public market valuations for AI infrastructure and frontier model companies, creating a benchmark against which every private company in the ecosystem will be measured. If they perform well at the opening, the entire private funding environment benefits. If they disappoint, the reverberations will be felt across the sector.

The structural bet underlying all of these valuations is that AI companies will generate the revenue to justify the multiples — and that the technology’s penetration into enterprise workflows will compound fast enough to make the current numbers look conservative in hindsight. That bet is not obviously wrong. But it has also not been proven at the scale now implied.

What It All Means

The AI investment landscape in 2026 tells a coherent story if you step back far enough to see the pattern.

The frontier labs are becoming infrastructure, and their capital requirements reflect that. The infrastructure layer — compute, data centres, power — is being built at a scale that assumes AI becomes as fundamental to the economy as electricity. The vertical AI companies are finding defensible positions in the gaps that generic models can’t fill. The horizontal “AI for everything” plays are facing increasing competition from the labs they’re built on.

For entrepreneurs, the lesson is clear: differentiation through vertical depth and proprietary data is the defensible path. Being a better interface on top of GPT-5 is not.

For investors, the concentration at the top continues — and the premium on companies with genuine moats grows with every capability release from the frontier labs.

For everyone else watching this ecosystem: the pace is genuinely extraordinary. OpenAI went from $300 billion to $840 billion in post-money valuation in roughly twelve months. The humanoid robotics category went from science fiction to $14 billion in commercial orders in roughly eighteen months. Whatever AI looked like two years ago, it does not look like that now.

And whatever it looks like today, it will not look like this in two years.