Andreessen Horowitz is reportedly raising $20 billion for US AI investments — a fund that would dwarf anything in venture capital history. The money is extraordinary. The question is whether it’s going to the right places — or inflating a category that’s bifurcated between genuine innovation and expensive demos.

Let’s put $20 billion in context for a moment.

The largest individual VC fund ever raised was SoftBank’s Vision Fund 2 at $56 billion — but that was backed primarily by sovereign wealth funds and took several years to deploy. A single firm raising $20 billion in a single fund, targeting a single category (US AI startups), would be the most concentrated bet on a single technology sector in venture capital history.

Andreessen Horowitz is reportedly doing exactly that. The fund is still in formation as of June 2026, but the reporting is consistent: a16z is seeking $20 billion from institutional investors to deploy into US-based AI startups, on the thesis that the current moment — AI moving from experimentation to infrastructure — represents a generational investment opportunity.

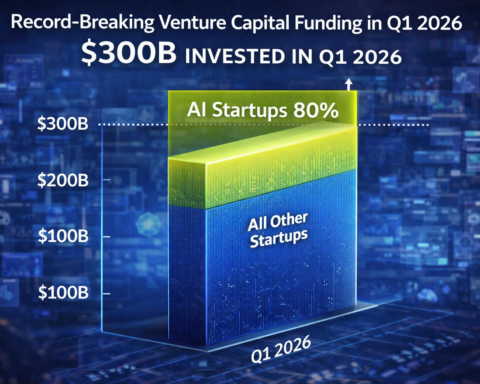

The same week this was being reported, SignalFire announced a $1 billion fund dedicated to AI startups, a more conventionally-sized bet that nonetheless underscores how serious institutional capital is treating the category. AI startups now attract 33% of total global venture capital. In Q1 2026 alone, they attracted $242 billion of the $300 billion that flowed into startups globally — 80% of all venture capital in the most active quarter in VC history.

These numbers are either the most obvious investment opportunity of the century or the setup for the most expensive venture capital bust since the dot-com collapse. Possibly both, depending on which layer of the stack you’re investing in.

What $20 Billion Actually Buys in 2026

The a16z fund, if it closes at reported size, would deploy approximately $2-4 billion per year over a 5-6 year fund life. At that deployment pace, it’s not primarily funding seed-stage startups. It’s funding the $100 million-to-billion-dollar growth rounds where AI companies with demonstrated revenue need capital to scale infrastructure, hire enterprise sales teams, and defend market positions against the foundation model providers expanding their native capabilities.

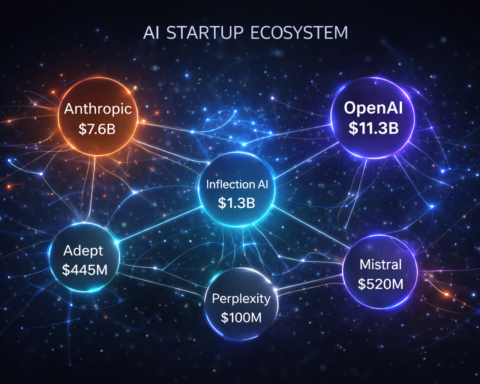

This is where the investment thesis gets interesting. The companies that need $100 million-plus growth capital in 2026 are mostly not the ones competing at the frontier model level — that’s OpenAI ($122 billion raised), Anthropic ($64 billion raised), and a small number of others. The companies raising growth rounds are the ones building on top of the foundation models: the vertical AI applications, the enterprise workflow tools, the AI-enabled professional services platforms.

The specific companies already capturing attention this year:

Cursor hit a $3 billion valuation on the strength of its AI-native IDE product. Fortune covered it as one of the fastest-growing software companies in history — from zero to $100 million ARR in less than two years. At $3 billion, the valuation implies significant future growth that requires continued model improvements, continued developer adoption at current rates, and no catastrophic disruption from Copilot or Claude Code eating its market share. All three of those are real risks. Cursor’s 72% autocomplete acceptance rate and genuine developer love are equally real.

Manus raised $1 billion specifically to build independent AI infrastructure outside Meta’s ecosystem. The Manus story is interesting as a strategic bet: the round explicitly signals that investors believe there’s value in AI infrastructure that isn’t dependent on the hyperscaler ecosystem, that Meta’s dominance in open-source AI (through Llama) creates a strategic risk for companies that build on it, and that building independence from that dependency is worth $1 billion of capital.

Perplexity reached $20 billion in valuation, crossed $200 million in annual recurring revenue, and is preparing for an IPO at an implied valuation that would make it one of the largest AI pure-plays to list. Its 780 million monthly queries represent a genuine alternative to Google Search for a meaningful user segment.

The Valuation Premium and What It Actually Means

Seed-stage AI startups command a 42% valuation premium over non-AI startups in 2026. Series A valuations for AI companies consistently achieve median valuations exceeding $50 million, compared to far lower benchmarks for comparable non-AI software companies.

The 42% premium reflects genuine expectations: AI markets are growing faster than traditional software markets, AI-enabled companies can often achieve better unit economics at scale, and the competitive dynamics of AI (proprietary data, compounding model improvements, switching costs from deep integrations) create winner-take-most dynamics that justify higher multiples.

It also reflects the possibility of a premium that’s at least partly disconnected from fundamentals. The category has been the subject of intense investor enthusiasm for three years. Valuations are set by competition between investors as much as by underlying business metrics. The seed-stage company that can tell a compelling AI story with minimal traction but a team with frontier model credentials can raise at prices that would have been unimaginable two years ago.

The honest signal in the data: seed-to-Series A conversion for AI startups has dropped from 24% to 18% in the past year. Investors are writing larger first checks but doing it for fewer companies. This is the market’s mechanism for managing the valuation inflation — quality bar for follow-on capital is rising even as the initial investment bar stays elevated.

For founders raising right now, this pattern has a practical implication. The seed is achievable if you can articulate the AI angle compellingly. The Series A requires demonstrated revenue and retention metrics — specifically $1 million or more in ARR and net revenue retention above 120% — that weren’t required two years ago. The market is separating stories from businesses, and it’s doing it at the Series A stage rather than waiting for Series B.

What the Money Is Not Solving

The AI VC ecosystem in 2026 has an allocation problem that the headline numbers obscure.

Research funding — the kind that produces foundational safety research, interpretability work, and the basic science that makes AI more reliable and more understandable — is not well-served by standard venture capital structures. VC funds invest for 10x returns on 5-7 year time horizons. Research that might produce safety methodologies in 3 years, which might improve model governance in 5 years, which might reduce catastrophic failure rates in 8 years — that’s not a venture capital investable. It’s a grant programme.

Anthropic has built something unusual: a company that does both commercial development and foundational safety research, partly because Dario Amodei’s mission conviction and partly because the commercial success has created the financial capacity to fund both. But this is not the norm. Most AI safety research depends on grants, academic funding, and the specific choices of a small number of mission-driven organisations.

The $20 billion a16z fund will fund companies that build on AI. It will not fund the research that makes AI safer to build on. The distinction matters more as the systems become more consequential.

Similarly: the capital concentrated at the top of the market — OpenAI, Anthropic, xAI consuming 65% of Q1 global VC in four rounds — creates a specific competitive environment for the rest of the ecosystem. The foundation models are being funded so aggressively that they can expand their native capabilities faster than any application-layer startup can defend against. Every feature that GPT-5.5 or Claude adds natively is a feature that a startup built and is now competing against with unlimited infrastructure budget.

The $20 billion fund is a bet that application-layer AI companies can survive and thrive in a world where the infrastructure providers have unlimited capital. It may be the right bet. History suggests that infrastructure dominance doesn’t always translate to application layer dominance — Microsoft didn’t win every category that ran on Windows. But the AI infrastructure providers are more directly competitive with their own ecosystem than Microsoft was, and the pace at which they’re adding native capabilities is faster than any previous technology transition.

The Honest Assessment of Where This Goes

The bifurcation that has emerged in AI venture is real and is getting more pronounced. The mega-rounds — four companies taking 65% of Q1 global VC — are in a different category from the broad-based seed and Series A activity that funds the actual diversity of the ecosystem.

The companies most worth funding in 2026, by the evidence available, are: companies with proprietary data assets that frontier models can’t access, companies with deep enterprise workflow integration that creates genuine switching costs, companies in regulated industries where the compliance moat creates defensibility, and companies building physical AI — robotics, industrial automation, autonomous systems — where the software-hardware integration creates differentiation that purely software players can’t replicate.

The $20 billion a16z fund, if deployed wisely against these criteria, would be funding durable businesses. If deployed against the thesis that anything with “AI” in the pitch deck deserves a premium valuation, it would be recapitulating SoftBank’s Vision Fund pattern — enormous capital allocations that inflated entire categories and produced disappointing aggregate returns alongside a handful of exceptional winners.

The distinction is not knowable in advance. What is knowable is that the founders who build businesses with real revenue, real switching costs, and real plans for surviving in a world where foundation model providers keep expanding — those are the companies that will still be around when the next correction comes.

And corrections in markets that have seen 80% of all venture capital concentrated in a single category always come. The question is just when, and which companies they find standing.