$300 billion. In one quarter. That’s not a typo, and it’s not evenly distributed. Here’s the honest story of Q1 2026’s record-shattering venture capital data — who got the money, who didn’t, and what this bifurcated market means for the thousands of AI startups that weren’t OpenAI.

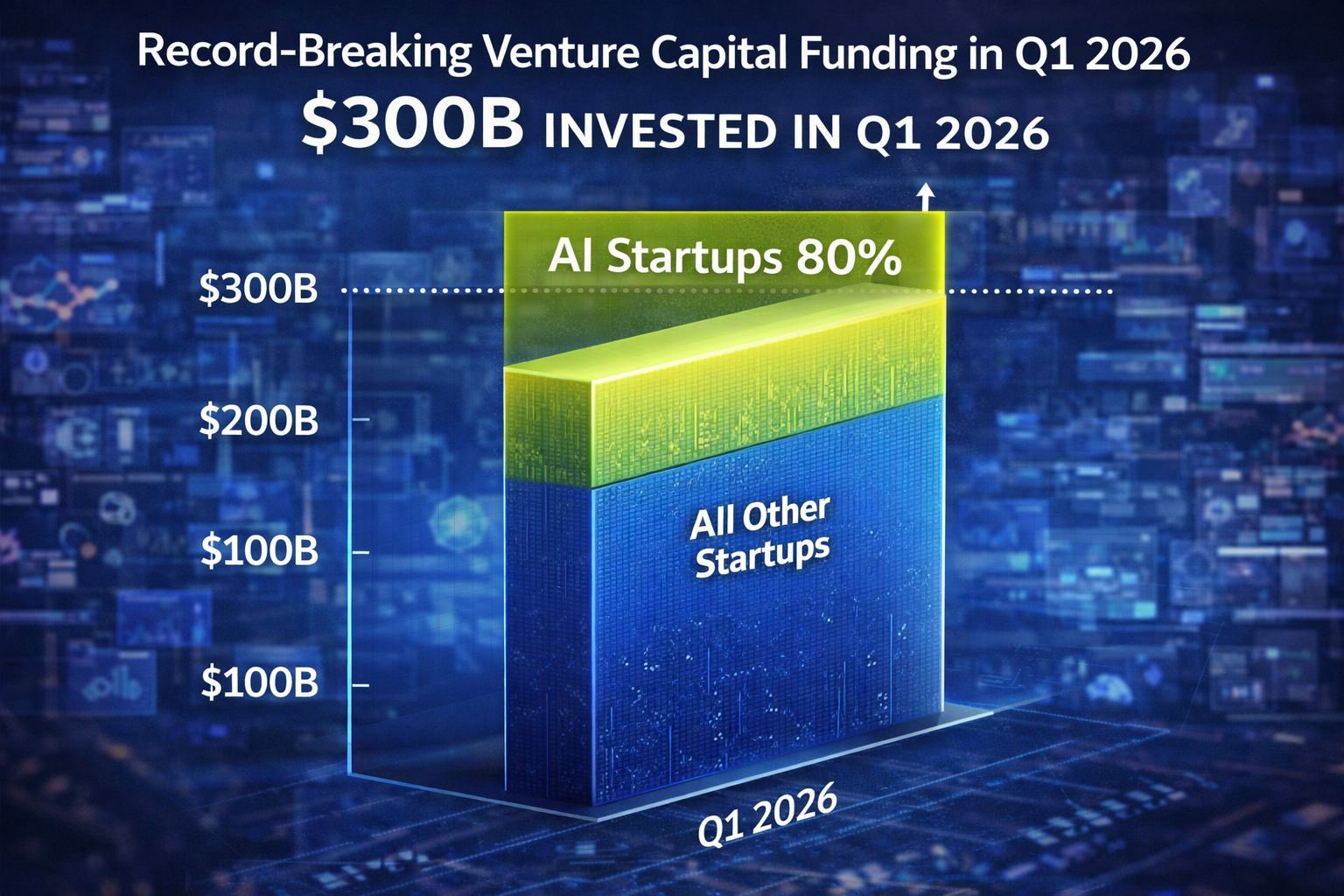

Let’s start with the number that broke every record on the books: $300 billion poured into startups globally in the first quarter of 2026. One quarter. That’s more than 70% of all venture capital spending in all of 2025 crammed into three months. It tops every full-year investment total before 2018.

That number generated predictable headlines about an AI funding boom, an AI renaissance, an AI supercycle. And in one narrow sense, it’s all of those things. In a broader, more honest sense, it’s a story about four companies, a K-shaped market, and what happens when capital gets so concentrated that the aggregate figures stop telling you anything useful about the ecosystem they claim to describe.

Let me walk through what actually happened.

The Four Deals That Made the Quarter

Four rounds absorbed $188 billion — 65% of the entire global venture market — in Q1 2026. They are the five largest private funding rounds ever recorded, minus one, and they all closed in a single three-month window.

OpenAI: $122 billion at an $852 billion valuation. The single largest private funding round in history, closed March 31, 2026. The company generates $2 billion in monthly revenue ($24 billion annualised), has 900 million weekly active users, and over 1 million enterprise customers. Amazon was named the exclusive third-party cloud partner as part of a $50 billion commitment. For the first time, $3 billion was raised from individual retail investors through bank channels — a signal of the consumer-market confidence in the company’s trajectory toward its Q4 2026 IPO target near $1 trillion.

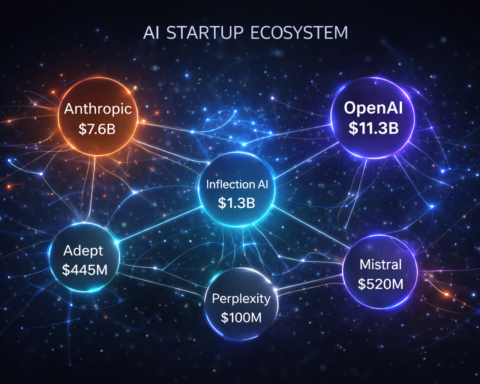

Anthropic: $30 billion at a $380 billion valuation (Series G). Closed February 2026, led by GIC and Coatue. The raise brought Anthropic’s total funding to nearly $64 billion since its 2021 founding. On April 7, 2026, the company announced annualised revenue surpassing $30 billion — exceeding OpenAI’s $25 billion for the first time (with the caveat that accounting methodologies differ between the two companies). Anthropic’s enterprise market share rose from 24.4% to 30.6% in March 2026 alone.

xAI: $20 billion Series E. Elon Musk’s AI company, parent of the Grok chatbot and X. Founded in 2023 and now sitting at $42.7 billion in total reported funding.

Waymo: $16 billion. The Alphabet-owned autonomous vehicle unit, reflecting a parallel boom in physical AI investment that deserves its own discussion.

Together: $188 billion. From four companies. In one quarter.

The Bifurcated Market Nobody Talks About

Here’s the part the headline numbers bury.

While late-stage funding surged 205% year-over-year, global startup deal count fell. More money, fewer deals. The Crunchbase Unicorn Board now includes roughly 1,700 companies. Of those, only about 40 have raised new funding or valuations since the beginning of 2024. The other 60% are still priced off an earlier cycle.

Peter Walker at Carta put it plainly: “While funding rounds have gotten slightly harder to raise, the capital for each round has increased. So fewer bets, but more capital.” AI startups are raising bigger rounds not because they have large teams — they often don’t — but because the cost of running frontier AI models at scale is genuinely enormous.

The seed-to-Series A conversion rate for AI startups is now approximately 18%, down from 24% in 2024. Investors demand $1 million or more in annual recurring revenue, net revenue retention above 120%, and a competitive moat that goes beyond a wrapper around OpenAI’s API. Miss those benchmarks and you get silence from Sand Hill Road.

There are roughly 70,000 AI companies globally. The vast majority are nowhere near the capital flood that Q1’s numbers describe. For every OpenAI raising $122 billion, there are thousands of startups burning through seed capital trying to find product-market fit in a landscape where the foundation model providers keep expanding their native capabilities.

One statistic crystallises the challenge: 40% of the AI startups founded in 2024 were shut down or significantly restructured by early 2026. That’s not catastrophic by startup standards — general failure rates at 24 months are 50-60% — but it underscores that the funding boom at the top of the market is not a rising tide lifting all boats.

The Unicorn Board: What $900 Billion in New Value Looks Like

The Crunchbase Unicorn Board added $900 billion in aggregate value during Q1 2026 — the largest single-quarter valuation increase ever recorded. Approximately 50% of tech unicorns in 2026 are AI-related startups.

The companies that benefited most are the ones that figured out, before the current cycle accelerated, that foundation model capabilities would increasingly commoditise application-layer features. The ones building directly on proprietary data, deep enterprise integration, or genuinely scarce capabilities — compute infrastructure, physical AI systems, specialised vertical AI — have held valuations and attracted fresh capital.

The ones that built wrappers got wrapped.

That’s the uncomfortable truth underneath the unicorn numbers: the methodology for building durable AI companies is becoming clearer, and it’s demanding. Proprietary data that foundation model providers can’t acquire. Enterprise distribution that creates switching costs. Regulatory moats in domains where compliance is a barrier to entry. Physical integration where the AI is inseparable from the hardware.

Several categories are attracting serious institutional conviction beyond the frontier lab megarounds: defence AI (Shield AI raised $1.5 billion, Anduril is targeting $60 billion in valuation), AI compute infrastructure (Nscale $2 billion, CoreWeave already public), voice AI (ElevenLabs at an $11 billion valuation), and autonomous vehicles (Waymo’s $16 billion round puts it at $126 billion).

The Strategic Investors Are Everywhere — Read the Fine Print

One shift that most startup funding stories underplay: corporate venture capital now represents 43% of AI startup funding, up from 31% in 2023.

Google Ventures, Microsoft’s M12, Nvidia’s NVentures, Salesforce Ventures, and Amazon’s Alexa Fund have all ramped up AI deal activity significantly. As has sovereign wealth capital from Saudi Arabia’s PIF, Abu Dhabi’s Mubadala and MGX, Singapore’s GIC and Temasek — all writing nine-figure cheques into AI rounds.

Strategic money brings strategic strings. These investors are optimising for ecosystem lock-in, distribution access, and data partnerships — not just financial returns. A startup that takes Nvidia investment often gets preferred access to GPU allocation. A startup that takes Microsoft money often finds itself with a path to Azure distribution. These are genuinely valuable. They also come with relationship dynamics that are harder to exit than a traditional VC relationship.

For founders evaluating term sheets in 2026, the identity of the investor is as important as the valuation.

What Q1 2026 Actually Tells You

Strip out the four mega-rounds and global venture activity looked roughly like Q4 2025 — healthy, growing, with competitive early-stage dynamics in AI. The $300 billion headline is real, but it’s 65% concentrated in companies that are already pre-IPO giants, not representative of the broader startup ecosystem.

The honest story is more interesting than either the boom narrative or the skeptical pushback. The AI funding market in 2026 is genuinely K-shaped: extraordinary at the frontier, competitive and difficult in the middle, and unforgiving at the bottom for companies that built features rather than businesses.

For founders, the lesson is less about “how do I get a piece of the $300 billion” and more about “what kind of company survives in a market where foundation model providers are expanding their native capabilities every quarter.” The answer keeps coming back to the same things: proprietary data, genuine enterprise integration, physical-world deployment, or deep vertical specialisation in domains the big labs won’t prioritise.

Those are harder to build than a well-designed API wrapper. They’re also harder to kill.