Anthropic’s annualised revenue surpassed $30 billion in April 2026, surpassing OpenAI for the first time. An October IPO targeting $60+ billion in fresh capital is reportedly in motion. Eight of the Fortune 10 are paying customers. Here’s what’s really driving this — and what it means.

Dario Amodei left OpenAI in 2021 with seven colleagues and a thesis: that building safe AI and building commercially successful AI were not in tension but were, in fact, the same project. The safest AI would be the most trustworthy AI, which would be the most deployable AI in the high-stakes enterprise contexts where the real economic value was going to be captured.

Three and a half years later, on April 7, 2026, that thesis produced a milestone that Silicon Valley wasn’t quite expecting on this timeline: Anthropic announced annualised revenue exceeding $30 billion, surpassing OpenAI’s approximately $25 billion for the first time.

The number needs some caveats — which we’ll get to — but the underlying trend it reflects is real and significant. And with an October IPO reportedly in motion, the race between these two companies is now the defining corporate drama in the most important technology sector of this generation.

The Revenue Story: What the Numbers Actually Say

Anthropic’s $30 billion annualised revenue figure is striking, but context matters.

The two companies use different accounting methodologies. Anthropic uses the gross method — counting the full amount charged to customers as revenue. OpenAI uses the net method — counting only its share of revenue after partner arrangements. If calculated under the same standards, Anthropic’s actual revenue scale may still be below OpenAI’s. The accounting methodology difference is real and worth keeping in mind.

That said, the enterprise adoption story is unambiguous. Enterprise customers spending more than $1 million annually on Anthropic doubled from approximately 500 in February 2026 to over 1,000 by early April — in two months. Eight of the Fortune 10 are paying customers. Enterprise revenue represents approximately 80% of Anthropic’s total.

Enterprise market share data from Ramp, which tracks AI spending across corporate expense systems, tells the competitive story most clearly: in March 2026, Anthropic’s share of the enterprise AI market rose from 24.4% to 30.6% — a 6.3 percentage point increase in a single month. During the same period, OpenAI’s market share declined from approximately 46% to 35.2%, narrowing the gap from 11 percentage points to 4.6 points. In competitive wins against OpenAI for new enterprise customers, Anthropic’s win rate reached 70%.

Why Enterprises Are Choosing Claude

The enterprise preference for Claude over ChatGPT isn’t primarily about benchmark performance — both models are extraordinarily capable and regularly trading the top position on various evaluations. It’s about something that sounds mundane until you’re the CISO at a Fortune 500 company: reliability, predictability, and safety.

Anthropic built its constitutional AI approach from the ground up to make Claude’s behaviour more consistent, more predictable, and less likely to produce the kind of unexpected outputs that create enterprise risk. When a financial services company is deploying an AI agent that touches client data and makes recommendations, they care enormously about the model behaving within expected parameters and not hallucinating in ways that create liability.

Claude Code’s 54% market share in the AI programming tool segment, with annualised revenue surpassing $2.5 billion, reflects this dynamic. Developers trust it with consequential output — production code, not just prototypes. Professional services firms, finance companies, and software organisations — the three industries with the highest AI penetration rates — all show Anthropic leading in market share.

The enterprise distribution advantage also shows up in the partnership structure. Anthropic’s Amazon relationship runs deep: Amazon’s $50 billion investment in Anthropic includes AWS as a primary cloud infrastructure partner, which means enterprises already running on AWS have a natural path to Claude integration that doesn’t require a new vendor relationship.

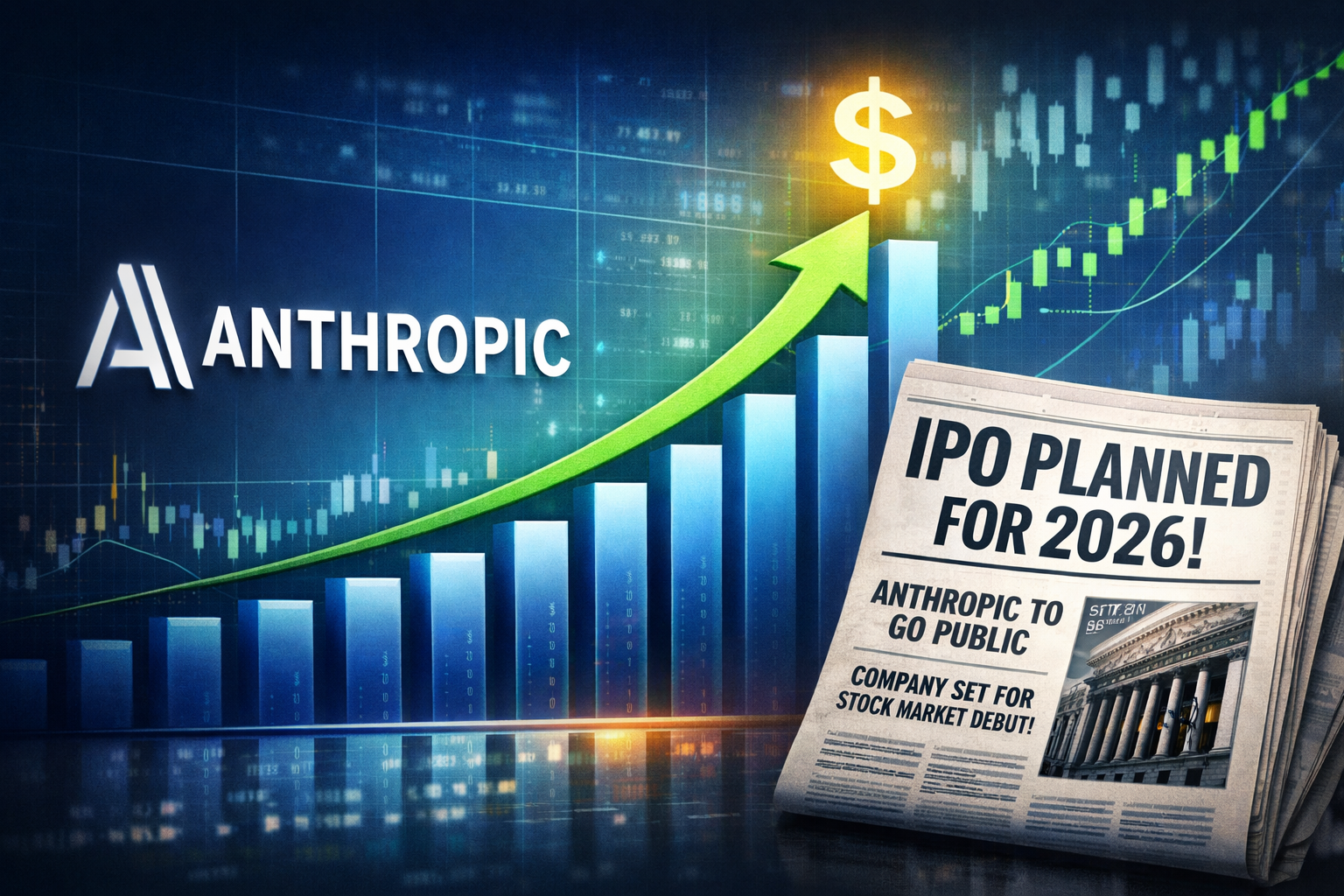

The IPO: What We Know and What We Don’t

Multiple reports, citing Bloomberg and other sources, indicate Anthropic is evaluating a US public listing as early as October 2026, targeting over $60 billion in fresh capital.

The board moves are happening that typically precede an IPO. Former Microsoft CFO Chris Liddell — who led General Motors’ $23 billion IPO in 2010, the largest ever at the time — has joined the board. A $5-6 billion employee stock tender offer has been launched to clean up cap table complexity. Goldman Sachs, JPMorgan, and Morgan Stanley are the primary candidate underwriters.

On secondary trading platforms, Anthropic’s implied valuation has reached approximately $688 billion — up 75% from three months ago. Some VC firms have approached Anthropic with investment offers at valuations as high as $800 billion. The company hasn’t accepted new funding, which is itself a signal: you don’t turn down money unless you’re about to access much larger amounts through public markets.

The profitability question is the honest challenge. AI inference costs are substantial, and Anthropic’s gross margin, while dramatically improved from -94% in 2024, is expected to be around 40% in 2025 — below target. The compute requirement for running frontier models at scale doesn’t get cheaper just because revenue grows; it grows with usage. Anthropic has addressed the compute supply concern by securing 3.5 gigawatts of TPU capacity through agreements with Broadcom and Google starting in 2027, extending through 2031. That’s compute supply security through the decade.

The IPO also solves a structural employee liquidity problem. The company has exceptional talent — PhDs in ML, safety researchers, world-class engineers — many of whom have been working for equity that has no liquid market. An October IPO changes that calculation dramatically.

The Race: Anthropic vs. OpenAI for First-Mover Status

OpenAI CEO Sam Altman reportedly wants a Q4 2026 IPO. CFO Sarah Friar has expressed concerns that the company isn’t operationally ready and that slowing revenue growth might not yet support the five-year spending plan. The company began running ads for non-premium users in February as a step toward demonstrating profitability paths.

If Anthropic lists in October, it goes first — and the first large-model IPO sets a valuation benchmark that affects everything that follows. Both companies understand this.

The argument for Anthropic as the better IPO story for public investors is straightforward: enterprise-grade revenue at 80% of the total mix, lower consumer exposure than OpenAI’s 900 million weekly users, and a regulatory and safety positioning that plays well with institutional investors who have ESG mandates and risk committees. The argument for OpenAI is market dominance, brand recognition, and the simple fact that consumer mindshare at their scale is enormously difficult to replicate.

Both companies are preparing for the largest tech IPOs since Saudi Aramco. The IPO market is watching, and so is every AI founder with growth ambitions.

The Broader Implications

The Anthropic revenue story is not just a corporate finance narrative. It represents something more significant about how the AI market is maturing.

The hypothesis that enterprise buyers, not consumers, would drive AI’s first major monetisation wave is proving correct. Businesses that can calculate a clear ROI on AI spend are spending more, faster, and with longer contract commitments than consumers buying $20/month subscriptions. The B2B model compounds in ways the B2C model currently doesn’t.

Anthropic’s ascent also validates the thesis that safety research and commercial success are compatible. The company has published foundational work on mechanistic interpretability, Constitutional AI, and model behaviour — research that informs the enterprise trust argument. Being the company that takes AI safety seriously turned out to be a commercial advantage, not a constraint.

Whether the IPO delivers at the valuations secondary markets are pricing in depends on profitability trajectory over the next 18 months. That’s the honest uncertainty. Everything else — the revenue growth, the enterprise adoption, the competitive position — has been validated by market reality.

The bell might ring as early as October. When it does, it won’t just mark Anthropic’s debut. It’ll mark the moment the AI industry confronted what its giants are actually worth in the clear light of public market scrutiny.