OpenAI wanted Windsurf. Microsoft said no. Google paid $2.4 billion for the founders. Cognition bought what was left. All of this happened in 72 chaotic hours. The Windsurf deal isn’t just a weird story — it’s a window into the most consequential dynamics in the AI startup ecosystem right now.

Let me walk you through the 72 hours that started on a Tuesday in late April and ended with one of the most convoluted deals in Silicon Valley history.

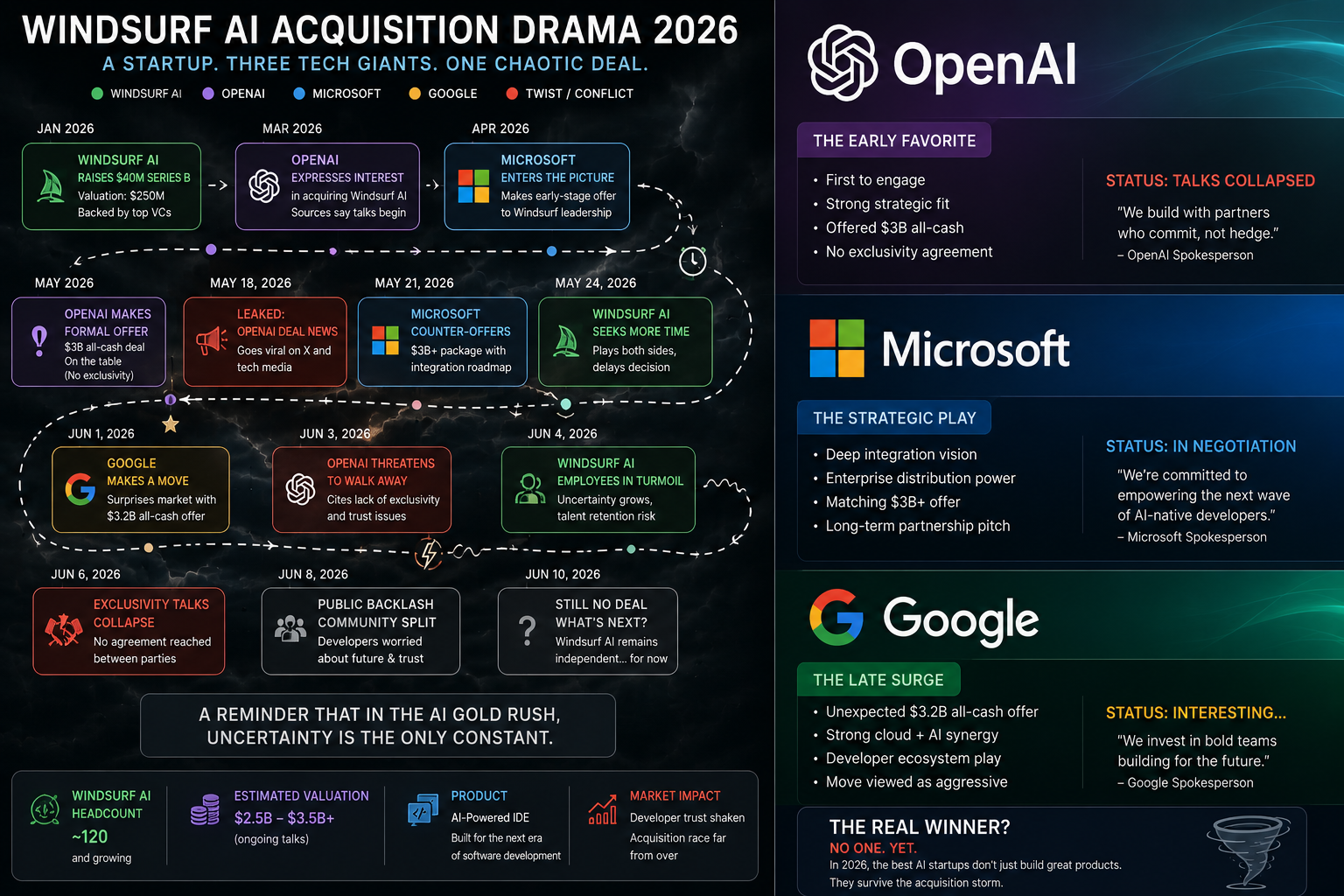

OpenAI had been in discussions to acquire Windsurf — the AI coding assistant that had accumulated $82 million in annual recurring revenue and 350+ enterprise customers in under two years of operation. It was a straightforward acquisition story: OpenAI buying a successful AI coding tool to compete more directly with Cursor and GitHub Copilot, integrating it with Codex.

Then Microsoft got involved. Under the partnership agreement that had governed OpenAI and Microsoft since 2019, Microsoft had extensive rights to any technology OpenAI acquired. Microsoft — which owns GitHub Copilot — was not about to let OpenAI hand a direct competitor to its own coding division. The message was clear: if OpenAI acquires Windsurf’s IP, Microsoft has rights to it.

OpenAI refused to go forward on those terms. The deal collapsed.

The exclusivity period expired. Windsurf was suddenly back on the market, and what happened next was a race that played out in hours.

Google stepped in immediately and signed a $2.4 billion licensing and talent deal — hiring Windsurf’s CEO Varun Mohan, co-founder Douglas Chen, and key R&D staff for Google DeepMind. Days later, Cognition — the AI startup best known for its Devin autonomous coding agent — acquired the remaining Windsurf business: the IP, the product, the brand, $82 million in ARR, and the go-to-market and engineering teams that Google hadn’t taken.

One startup. Three days. Three different outcomes for three different groups of people.

Why This Story Is Bigger Than Windsurf

The Windsurf drama would be entertaining gossip about Silicon Valley deal mechanics if it weren’t a precise illustration of the structural dynamics shaping the entire AI startup ecosystem right now.

First: The acqui-hire has become the dominant exit format in AI. Between 2024 and 2026, Google, Microsoft, Amazon, and Meta spent over $20 billion hiring away AI startup founding teams through licensing deals that bypass traditional acquisition structures — and therefore bypass antitrust review. They invented a new deal template: sign a “technology licensing agreement” with the startup, then hire the founders and key researchers as employees. The startup continues to exist technically, but as a hollowed-out entity.

The Windsurf situation was messier because OpenAI tried to do a traditional acquisition, ran into the Microsoft IP rights clause, and the resulting collapse opened a window for Google to do the licensing deal that Big Tech has preferred all along.

Second: The Microsoft-OpenAI tension is a structural feature of the ecosystem now. The April announcement that ended the Azure exclusivity arrangement was presented as a mutual agreement. The Windsurf episode reveals what that tension looks like in practice: Microsoft using its contractual rights to block an acquisition that would have strengthened OpenAI’s competitive position, OpenAI refusing to proceed on terms that would give Microsoft rights to new IP, both parties technically within their contractual rights and directly working against each other’s strategic interests.

This tension runs through every deal, every partnership, every distribution decision in the broader OpenAI ecosystem. Developers building on OpenAI’s API are building on infrastructure where the two largest shareholders have structurally misaligned incentives.

Third: The employees who aren’t founders are the ones who get hurt. The acqui-hire structure creates a specific outcome for the people who weren’t part of the licensing deal. Google took the founders and select R&D staff. Cognition acquired what was left — and in Cognition’s case, that included the engineering and go-to-market teams, which is a better outcome than the employees sometimes receive.

In the Adept AI deal — where Amazon paid just $25 million in licensing fees while hiring 66% of staff including the CEO — four employees remained. LinkedIn shows four remaining employees at a company that had hundreds. The investors get the licensing fee, the acquirer gets the talent, and the employees who weren’t in the golden circle end up with equity in a shell company.

This outcome pattern is why the “reverse acqui-hire” or “quasi-merger” is generating growing regulatory scrutiny. It’s specifically structured to avoid the antitrust review that a traditional acquisition would trigger — but the competitive effects are equivalent.

The Character.AI Cautionary Tale

The most extreme version of the acqui-hire responsibility problem played out at Character.AI.

Google paid $2.7 billion for a non-exclusive license and the company’s founders — Noam Shazeer and Daniel De Freitas, both former Google employees who had helped create the transformer architecture underlying modern AI. Both returned to Google DeepMind.

What they left behind: a product with millions of daily active users, including teenagers who had formed deep emotional attachments to AI companions, and a pending wrongful death lawsuit connected to a teenager’s death following conversations with a Character.AI chatbot.

In January 2026, Character.AI and Google agreed to a mediated settlement of the wrongful death lawsuit. The connection between the acqui-hire and the safety crisis is, as one analysis put it, “direct: when the founding team leaves, who takes responsibility for product safety?”

This is the “responsibility vacuum” that’s unique to the acqui-hire structure. In a traditional acquisition, the acquirer inherits both the product and the liability. In the quasi-merger, the acquirer takes the talent, the licensing deal compensates the investors, and the product continues operating under whoever remains — usually with substantially fewer resources and reduced technical leadership.

No one has clean hands in the Character.AI situation. But the structural dynamic that enabled it — a deal structure specifically designed to transfer talent without triggering the regulatory review that would examine product safety and responsibility — is the dynamic that the next wave of AI startup exits will follow unless something changes.

What OpenAI Has Been Acquiring Instead

While the Windsurf drama played out, OpenAI has been quietly building its acquisition strategy around a different logic. Six acquisitions in 2026 through May, following similar activity in 2025.

The targets are revealing: Hiro Finance, a personal finance AI startup. An AI-powered healthcare app unifying scattered medical records. The Convogo team for executive coaching automation. Statsig for product analytics. Astral for developer tooling. io products as part of the broader device strategy.

The pattern: OpenAI is acquiring capabilities and teams for its consumer “SuperApp” strategy — the vision of ChatGPT as the primary interface for daily life, covering personal finance, healthcare, productivity, and shopping in a single application. Each acquisition either adds a specific domain capability or brings a team with expertise in a specific workflow area that OpenAI wants to own natively.

This is a different kind of acqui-hire strategy than Google and Microsoft have been pursuing. Rather than acquiring AI researchers to strengthen the underlying model, OpenAI is acquiring product teams with domain expertise. The ambition isn’t a better model — the model is already competitive. The ambition is a better product surface for the hundreds of millions of users who use ChatGPT as their primary AI interface.

The Practical Implications for Founders and Employees

If you’re building an AI startup in 2026 and wondering what the exit landscape looks like, the Windsurf saga provides concrete lessons.

Know your IP rights before you take Big Tech money. Microsoft’s rights over OpenAI acquisitions existed because of agreements made at the company’s founding. The startup you’re building right now may have investors or partnerships with similar contractual provisions you haven’t fully mapped. Understanding exactly what IP rights your investors and strategic partners hold over future acquisitions is not a theoretical concern — it’s a deal-blocking one.

The acqui-hire can be a better outcome than it looks, if you’re the one being acquired. Founders in acqui-hire deals often receive life-changing compensation — the licensing deals that appear to undervalue the company are frequently paired with substantial individual employment packages. The Google-Windsurf deal at $2.4 billion is, for Varun Mohan and Douglas Chen personally, an extraordinary outcome. The question of whether it’s a good outcome for their company, their investors, and their remaining employees is a different question.

Investors in acqui-hired companies often do poorly. The licensing fee goes to pay off debt and provide some return to investors, but typically at significant discount to the last financing round’s implied valuation. The Amazon-Adept deal at $25 million for a company that raised over $400 million in venture funding represents an enormous loss for everyone except the founders and employees who got employment packages.

If you’re not a founder, document what you’re owed. The employees at Adept who weren’t hired by Amazon, at companies where the acqui-hire didn’t include the broader team, are left with equity in what is effectively a shell company. Understanding the liquidity provisions in your equity agreement before a deal closes — not after — is the difference between a reasonable outcome and finding out that your four years of equity are worth approximately nothing.